SMM June 27:

Tin prices were boosted by slower-than-expected production resumptions in Myanmar's Wa State and supply tightness caused by Thailand's restrictions on Myanmar tin ore transit. Rare earth permanent magnets gained policy-driven momentum, with industry chain participants expressing optimism about the rare earth market outlook. Tungsten prices continued hovering at high levels. Rapid development in downstream sectors like new energy, semiconductors, and defense industries strengthened growth expectations for minor metal demand. Market capital's favor towards resource-scarce varieties also contributed to the sector's strength. As of 14:34 on June 27, the minor metal sector rose 1.98%, with Huayang New Materials hitting the limit-up, while Poco New Materials, Yunnan Tin, Sinomag Technology, Earth-Panda, and CMOC led gains.

News

Huayang New Materials announced on June 25 that its related party Huayang Group received an investigation notice from the China Securities Regulatory Commission. The notice stated Huayang Group was being investigated for occupying funds from Yangmei Chemical in 2021 without properly disclosing non-operational capital transactions. The company clarified this incident is unrelated to its operations and won't affect normal production activities, confirming no fund occupation by controlling shareholders or related parties. The event has no direct operational impact. After achieving "four limit-ups in five trading days," Huayang New Materials issued a stock trading abnormal fluctuation warning on June 18, noting its shares had accumulated a 20% price deviation over three consecutive trading days (June 13, 16, and 17, 2025) per SSE regulations. Recent volatile stock movements significantly outpaced industry trends. The company reiterated it has no rare earth permanent magnet business, focusing instead on platinum-group metal recycling, where rising precious metal prices are increasing raw material procurement costs.

Spot Market

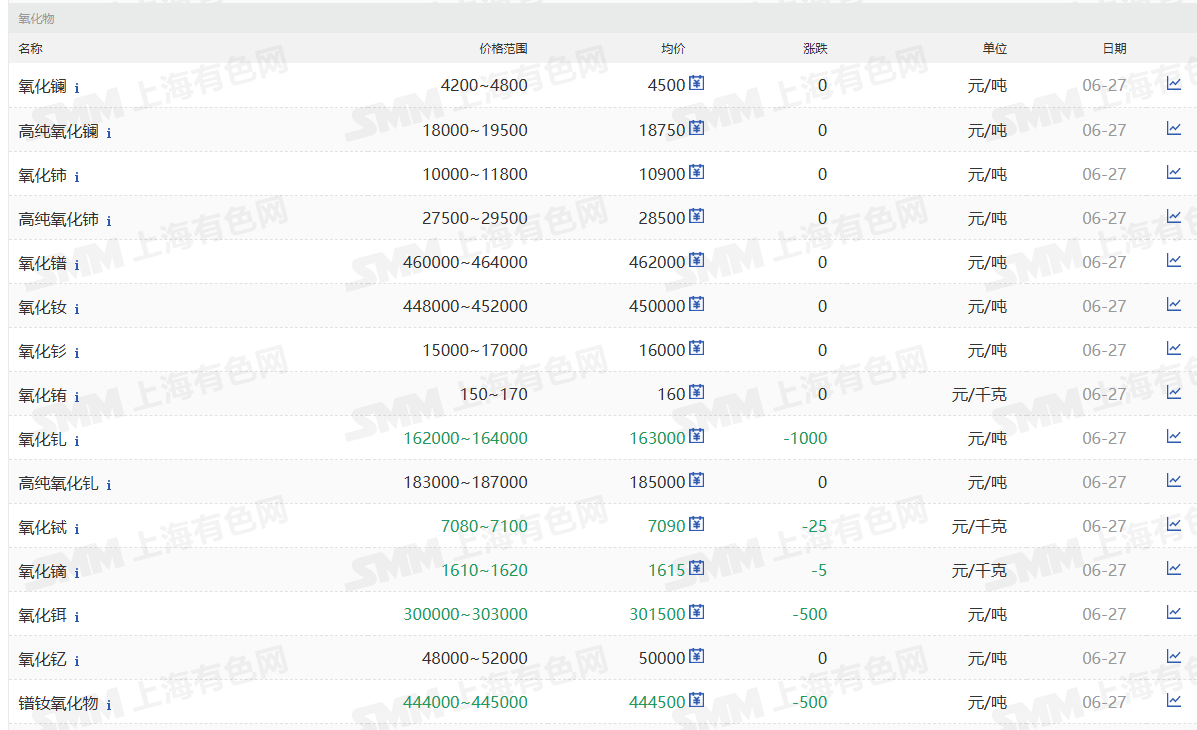

Rare earth spot:

》Click for SMM rare earth spot prices

》Subscribe for SMM metal spot historical price trends

On June 27, SMM's Pr-Nd oxide (1#) quotation range stood at 444,000-445,000 yuan/mt, averaging 444,500 yuan/mt, down 0.11% from the previous trading day. Recently, due to the impact of the traditional rainy season in Southeast Asia, Myanmar's ore imports have declined significantly, and mine-end suppliers have shown weak willingness to sell. Rare earth oxides overall remain slightly in the doldrums, with sluggish inquiries from downstream buyers and some suppliers reducing prices to release small volumes. As downstream industries gradually emerge from the traditional off-season, coupled with frequent positive market news, most industry insiders hold optimistic expectations for future rare earth prices. Under this market sentiment, low-priced cargoes may become even harder to find. Overall, while the rare earth market faces short-term volatility challenges, the industry maintains a generally positive outlook on its long-term development prospects.

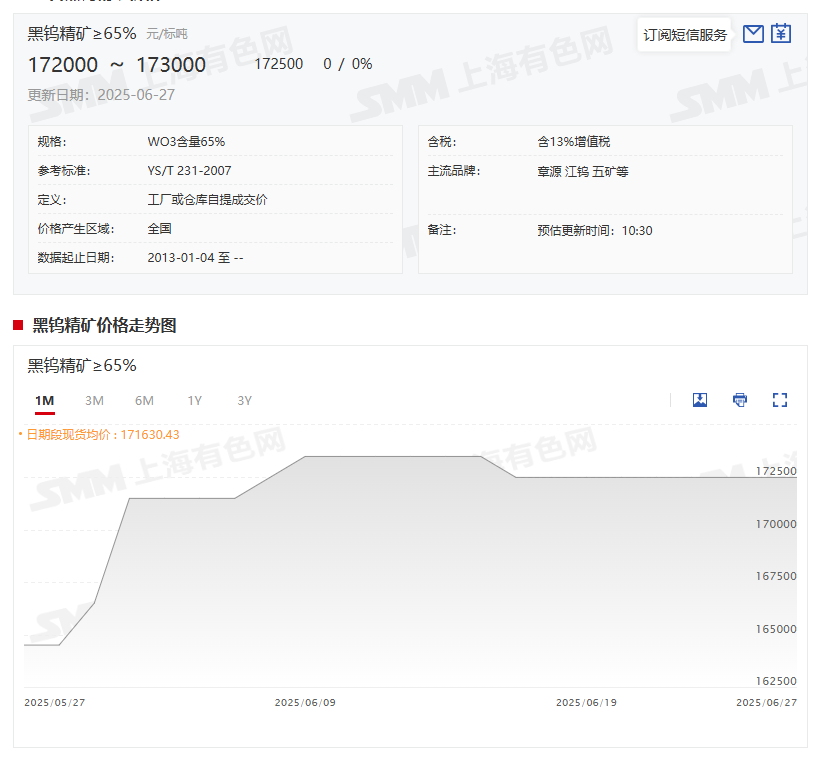

Tungsten spot market:

》Click to view SMM tungsten spot prices

》Subscribe to view SMM metal spot price history

On June 27, the tungsten market primarily exhibited high-level consolidation, with mainstream mine-end suppliers maintaining low inventory levels and insufficient willingness to lower prices. Mine-end declines remained limited, and quotations stayed elevated. Downstream APT enterprises faced poor profitability, leading some smelters to implement production cuts and maintenance. The upstream primarily fulfilled long-term contract shipments, while downstream firms conducted just-in-time restocking, resulting in stable overall transactions. In the short term, macro factors include marginal easing of Middle East tensions and reduced overseas risk aversion. Fundamentals show a tight balance between domestic tungsten's upstream and downstream sectors. With upstream mine-end raw material inventories at low levels coupled with production controls, tungsten price corrections remain limited. Downstream smelters face poor profitability, creating a dual weakness in supply and demand. Structural contradictions in the industry chain are prominent, with a tug-of-war between longs and shorts as the market undergoes restructuring. Short-term maintenance of high-level consolidation is expected. Continued attention should be paid to mainstream companies' July long-term contract pricing and downstream operational rates.

Recommended readings:

》Rare earth prices continue to stabilize - How will market expectations evolve? [SMM Analysis]